New Housing Finance Recovery Rules

Pakistan is going through a major change in how banks deal with people who stop paying their home loans. The government has put forward new housing finance recovery rules for 90-day loan defaulters that give borrowers a fair chance to fix their situation before losing their home. This is not just a legal update — it is a shift in how the country thinks about mortgage lending and borrower protection at the same time.

For years, banks in Pakistan have been reluctant to give out home loans because there was no clear way to get their money back if someone defaulted. These new rules are meant to fix that problem. By giving banks a proper legal path to follow and giving borrowers enough time to respond, the government wants to build confidence on both sides of the table so that more families can finally afford to buy a home.

You Can Also Read: Pakistan to Replace 200-Unit Electricity Subsidy with BISP-Based Targeted Relief

What Exactly Are These New Recovery Rules About?

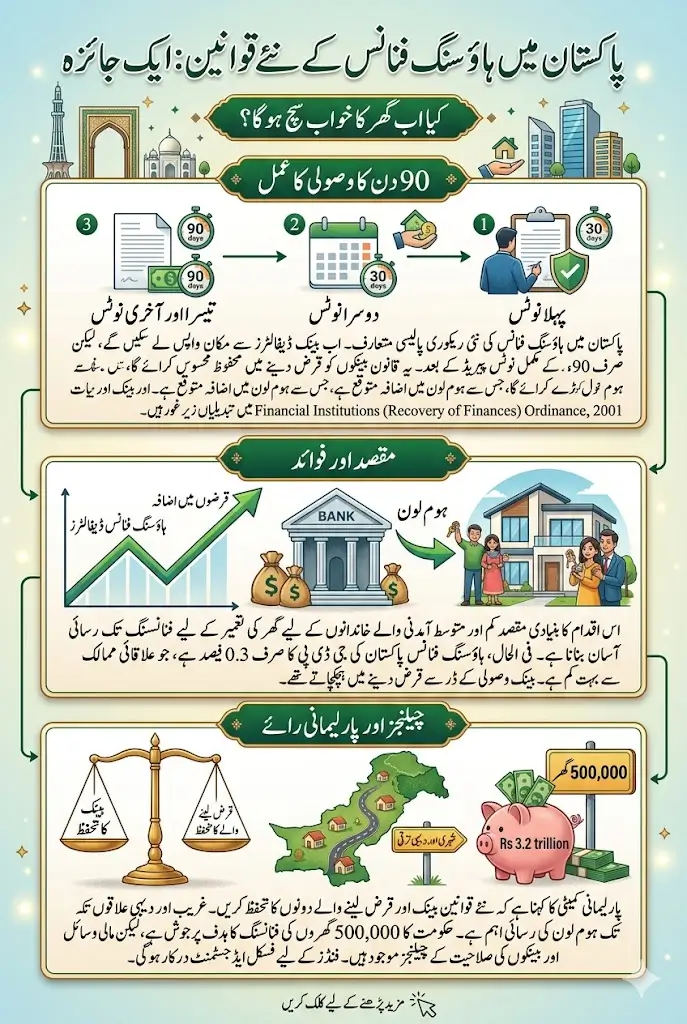

The new housing finance recovery rules for 90-day loan defaulters are simple in their structure. If a person fails to pay their mortgage, the bank must send three separate notices one every 30 days. Only after all three notices have been sent and ignored can the bank move ahead with selling the property.

This 90-day window is not just a formality. It gives the borrower real time to arrange funds, talk to the bank, or find another way out. The government made it clear that no bank can skip this process and go straight to taking the home.

Why the Government Decided to Make These Changes Now?

Pakistan’s housing finance sector has been weak for a long time. Mortgage loans make up only 0.3 percent of the country’s GDP and just 0.56 percent of total private sector credit. These figures are far behind other countries in the region, and the government knows it.

One of the biggest reasons banks have stayed away from mortgage lending is the absence of a strong recovery law. Without a clear legal framework, banks feared they would never get their money back from defaulters. These new rules are meant to remove that fear and push banks toward giving more home loans to deserving families.

You Can Also Read: CM Punjab Kisan Card: Only 3 Days Left to Qualify For Lucky Draw Rewards on Timely Loan Repayment

How the 90-Day Notice Period Works in Simple Terms?

The process is straightforward. When a borrower misses mortgage payments and the bank decides to act, it sends the first notice. If the borrower does not respond or pay within 30 days, a second notice goes out. After another 30 days of silence, the third and final notice is issued.

Once all three notices have been properly delivered and 90 days have passed with no payment, the bank can legally move to sell the mortgaged property. But even at that point, there is still a window where the bank and borrower can reach a new agreement before the sale actually happens.

What the Parliamentary Committee Said About These Rules?

The Standing Committee on Finance and Revenue did not simply wave this bill through. Members raised serious questions and pushed back on certain parts of the proposed law. Their main concern was that banks might end up with too much power and ordinary borrowers might have no real protection.

Committee Chairman Syed Naveed Qamar stressed that affordable housing must reach the people who actually need it most — low-income families who have never had access to formal home financing. He made it clear that any new law must protect both the bank and the borrower equally, not favour one side over the other.

You Can Also Read: Meta Introduces AI-Powered Age Verification In 2026

Concerns About Rural and Low-Income Borrowers

One issue that all committee members agreed on was the lack of access to housing finance for people in rural areas and informal employment. Most mortgage products in Pakistan are designed for salaried workers in cities. People who work in small businesses, agriculture, or daily labour have almost no way to qualify for a home loan.

The committee recommended that the State Bank of Pakistan and the government work together to create simpler loan procedures, more flexible income requirements, and stronger subsidies for households that fall outside the normal banking system. Without these steps, even the best recovery law will not help the people who need housing the most.

The Big Question — Can Pakistan Actually Finance 500,000 Homes in Four Years?

The government has set an ambitious target of financing 500,000 housing units over the next four years. To do this, an estimated Rs. 3.2 trillion in financing will be needed. However, Finance Secretary Imdadullah Bosal admitted in the committee meeting that the government currently does not have that kind of money available.

He said the funding will have to come through fiscal adjustments, and that existing subsidy schemes may need to be reviewed. Even the Public Sector Development Programme (PSDP) could be reduced to make room for housing finance spending. Committee members questioned whether banks even have the institutional capacity right now to handle such a large number of housing loans.

You Can Also Read: PAVE Program Phase 2 Vehicle Distribution Targets Set

What Needs to Happen for Housing Finance to Actually Work in Pakistan?

The committee gave some important recommendations to make housing finance more accessible to ordinary people. They asked the government and the State Bank of Pakistan to simplify the loan application process, create more flexible eligibility rules, and provide stronger subsidy support for low-income and informal-sector workers.

Members were also concerned about people in rural and underserved areas who currently have almost no access to mortgage finance. For these new rules to truly work, the benefits must reach beyond big cities and into smaller towns and villages where the housing shortage is just as serious.

FAQs

What are the new 90-day housing finance recovery rules in Pakistan?

The new rules allow banks to take back a mortgaged home only after sending three separate notices of 30 days each to the defaulting borrower. The bank cannot take any action until the full 90-day notice period is complete.

What is the PM Apna Ghar Programme and who can apply?

It is a government housing scheme for first-time homebuyers from low and middle-income families. It offers loans of up to Rs. 10 million at a 5 percent fixed rate for up to 20 years, with the bank covering 90 percent of the cost.

Can a borrower still save their home after receiving loan default notices?

Yes. Even after all three notices are issued, the bank can still offer to restructure or settle the loan before selling the property. Borrowers should immediately contact their bank and try to reach a new agreement.

Why is Pakistan’s housing finance sector so weak?

Mortgage financing in Pakistan is only 0.3 percent of GDP, which is very low. Banks have been reluctant to give long-term home loans because there was no strong legal framework for recovering money in case of default.

Did the National Assembly approve the new housing finance recovery law?

Not yet. The Standing Committee on Finance deferred the bill to its next meeting. A revised draft will be shared with committee members before any final approval is given.

You Can Also Read: BOP Offers 0% Markup Installment Plans on Honda and E-Turbo Bikes

Final Words

The new housing finance recovery rules for 90-day loan defaulters are a step in the right direction for Pakistan. If applied fairly, they can help banks lend more freely while keeping borrowers safe from sudden or unfair action on their homes.

The road ahead still needs careful planning, stronger support for low-income families, and honest implementation at every level. When all of that comes together, more Pakistani families may finally get the chance to own a home they can call their own.